This directory contains a complete implementation of the Log-Periodic Power Law Singularity (LPPLS) model for Bitcoin bubble detection and prediction, as described in LPPLS-model.md.

lppls_backtest.py - Main LPPLS model implementation with backtesting frameworklppls_usage_guide.py - Complete usage guide with examples and explanationslppls_comprehensive_demo.py - Comprehensive demonstration across different time periodsdemo_lppls.py - Simple demonstration scripttest_lppls.py - Basic functionality tests

from lppls_backtest import LPPLSBacktest

# Initialize the system

lppls = LPPLSBacktest()

# Run backtest on recent data

results = lppls.run_backtest(

start_date='2024-01-01',

end_date='2024-11-30',

window=10, # Days for slope calculation

tc_threshold=5, # Days before critical time for signals

slope_threshold=0.001 # Signal sensitivity

)

# Get future predictions

future_pred = lppls.predict_future(days_ahead=30)

The LPPLS model identifies financial bubbles by fitting price data to:

p(t) = A + B(tc - t)^m (1 + C * cos(ω * log(tc - t) + φ))

Where:

A: Final price level after bubbleB: Amplitude of power-law decaytc: Critical time (bubble peak/crash)m: Power-law exponent (0 < m < 1)C: Oscillation amplitudeω: Angular frequencyφ: Phase✅ LPPLS Model Fitting - Uses differential evolution optimization for robust parameter estimation

✅ Local Slopes Analysis - Calculates trend slopes over moving windows to enhance signal quality

✅ Signal Generation - Generates buy/sell signals when approaching critical times with favorable trends

✅ Backtesting Framework - Complete portfolio simulation with performance metrics

✅ Future Prediction - Extrapolates model to predict future prices and critical events

✅ Flexible Data Sources - Supports both yfinance API and local CSV data

✅ Comprehensive Analysis - Includes Sharpe ratio, max drawdown, and trade analysis

python lppls_usage_guide.py

python lppls_comprehensive_demo.py

python demo_lppls.py

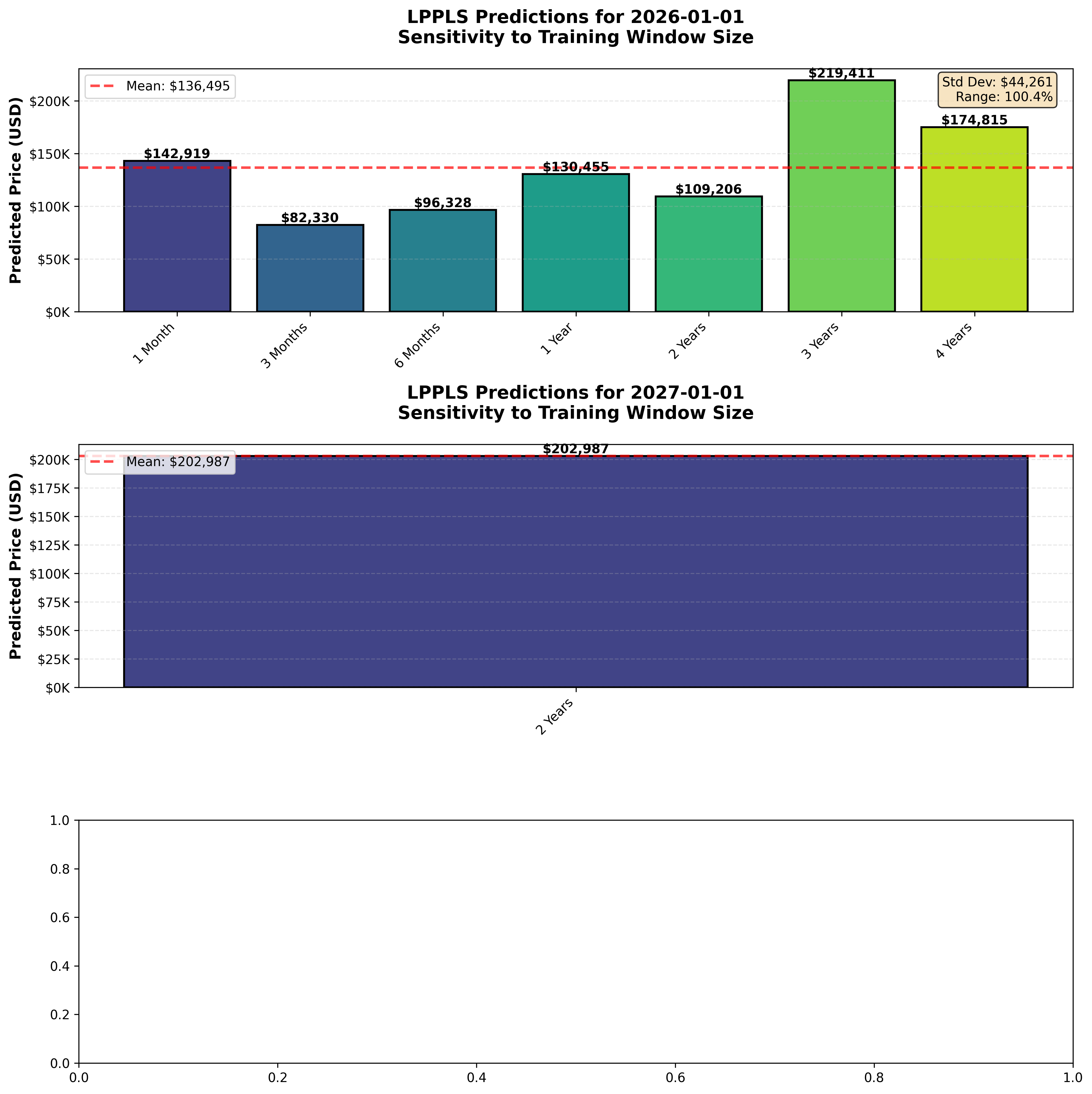

🔴 CRITICAL: Extreme Window Sensitivity Detected

The LPPLS model exhibits 100%+ prediction variance depending on training window size. A comprehensive sensitivity analysis (see full report) revealed:

⚠️ DO NOT use single LPPLS predictions for investment decisions!

Recommended approach:

See also:

⚠️ Best for Bubble Detection: Model designed for bubble periods, not general prediction

⚠️ Historical Data Required: Needs 100+ days for reliable fitting

⚠️ Parameter Sensitivity: Results depend on parameter choices (window size is the most critical)

⚠️ No Guarantees: Statistical model, not deterministic prediction

⚠️ Research Tool: Use for analysis, not standalone trading

Based on the work of:

scipy.optimize.differential_evolution for global optimizationPotential improvements:

For detailed technical information, see the original research documentation in LPPLS-model.md.

{kind=link}